In this second post on exit planning, we explore some of the key actions that underpin successful preparation (what we call Stage 1) before an intensive, competitive M&A sale process (Stage 2). Based on our experience across 300 exits spanning decades, we firmly believe that thoughtful, sustained preparation over several months or even 1-2 years before a company is formally put up for sale increases both the price and certainty of an eventual deal.

Yet in our experience less than 10% of successful growth companies undertake a sufficiently comprehensive Stage 1 effort. All too often boards, having decided formally to sell the company, hire a banker to market the business ‘competitively.’ As we highlighted in our first post, this is a key reason why half such sale processes fail; a company is immediately an asset for sale offering buyers a compressed timeframe to make a key strategic decision. Having successfully completed numerous Stage 1 + Stage 2 processes, we know first-hand how markedly better exits result from preparation before a full sale effort kicks off.

What are some key steps involved in a successful Stage 1? It’s important to point out that Stage 1 must be tailored to each company. Growth companies operate in such different segments, each with their own unique characteristics, making a ‘one size fits all’ approach impossible. What we can offer below is a partial list of some of the key steps we repeatedly see as critical to success (which we always define as achieving a higher valuation, greater certainty, or both during the formal sale process).

Set Up for Success

We often describe it this way: exit preparation should become a business process over a defined period. At its core, every company comprises a set of processes that operate efficiently to support growth. Exit preparation needs to become one such process. This means a small group is assigned (never full-time), clear oversight and responsibility allocated, goals set, and outcomes evaluated. Rarely does exit prep require more than three people, and never anywhere close to full-time. Our goal in working with these small teams within companies is to manage the entire effort to less than 10% of a CEO’s personal time. Any more than that is difficult to sustain. Simultaneously, a core part of any CEO’s job is achieving a successful exit, and in the months or years before that exit we would argue strongly that every CEO should invest this level of time towards a better outcome.

We find that CEOs often don’t invest the time because they are unsure WHERE to invest it. The most successful growth CEOs have typically delivered perhaps one, or at most a handful of successful exits in their careers. As each of our most senior people have completed over 100 exits, the value of this experience helps focus on the ‘best few’ actions for what is invariably a time-starved team. The second dimension is regular reviews with clear deliverables, ensuring that management and the board see how exit prep is developing every two to four weeks.

One often-overlooked aspect is a chairperson or board member with repeat exit experience. Adding someone to the CEO’s circle with this type of context, well before an exit, can only help a CEO navigate the process with confidence. While an unwritten part of our job is always acting as informal coaches to a CEO, we cannot entirely supplant someone who has familiarity and context for the business from the inside-out. Again, we find that too-often boards don’t consider exit experience as a core specification when adding a new board member, missing the opportunity to at least evaluate the potential benefits of that expertise.

Thinking About Performance

Virtually no strategic buyer cares solely about a growth company’s current numbers. What they nearly always care about far more is what they can do with the acquired company post-close. One of the biggest mistakes CEOs make in exit planning is to focus effort on refining forecasts in the way they have learnt when planning a funding round. In fact, what is FAR more important is that a company exceeds its near-term forecast by even a small margin. Put another way, a company achieving $45m in revenue having forecast $50m likely receives a lower valuation than it would forecasting $42m then achieving $43m.

This isn’t to say longer term forecasting is irrelevant; it is always a useful indicator of potential. But what CEOs regularly under-appreciate is the importance of risk reduction to even the best buyers. Strategics think at least as much about risk as about upside and potential. The highest value exits occur when a buyer is confident a company is both ‘exciting’ and ‘safe to buy.’ In the above example, exceeding a near-term forecast can mean a buyer grows confident enough to discount future performance less, which always leads to a higher exit price.

A related point is that post-deal, a growth company’s forecasts will no longer matter. As part of a larger group, success becomes all about leveraging a bigger opportunity together and expanding to a far bigger size than any growth company can credibly plan on its own. Again, a long-term forecast is always useful, but it is only one of several key ingredients, and companies who are accustomed to making ambitious forecasts need to use the exit prep phase to temper those if needed.

Creating a Story Not a Deck

Far too many companies’ sale memorandums are compendiums, failing to tell a compelling story. While compiling all the key information has its value, it does not sell a business for maximum price. A compelling exit ‘story,’ however, is fundamentally different from fundraise storytelling, as the target audience is entirely different (strategic buyers not investors) and often the growth company is also more mature or larger than when it last raised capital. All the elements that should go into effective story-telling for a strategic audience would likely fill several books, but we’d like to share a few guidelines we’ve seen work time and time again:

- Define what you do that is ‘hard’ – a key ingredient of a great story is anchoring the few things a company has done which even much larger companies find challenging. This could include redeveloping a complete fintech stack, breaking into an important but challenging market, signing one or more game-changing commercial deals, onboarding a difficult but high-value customer, or even maintaining very high customer satisfaction or sustained high-quality product releases. Parsing what is truly hard from what a company thinks is hard (there is always a difference) takes time and iteration but is core to any credible story.

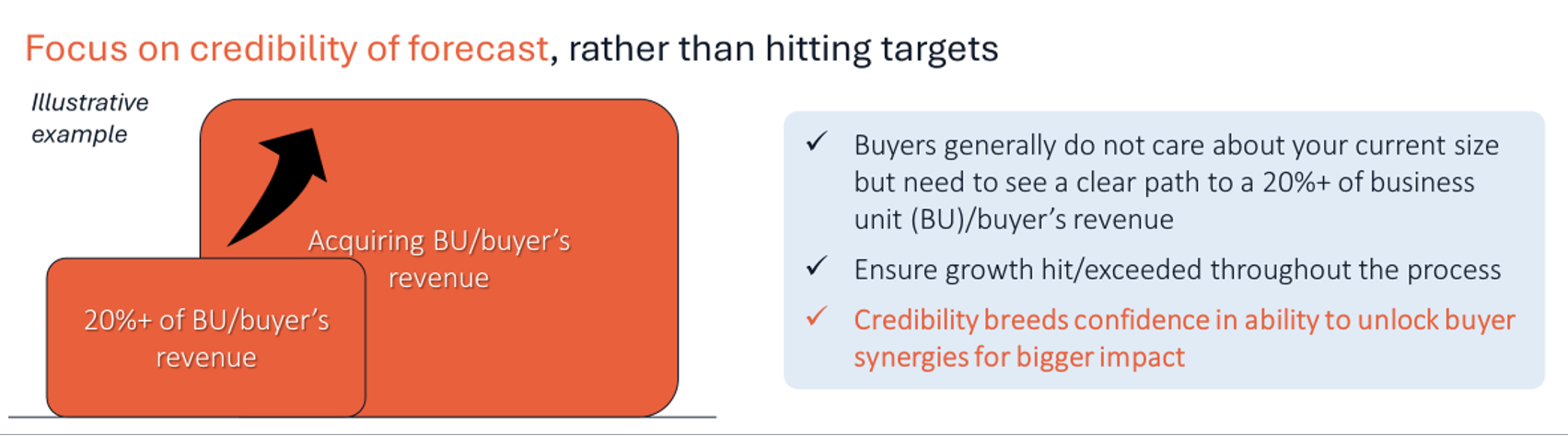

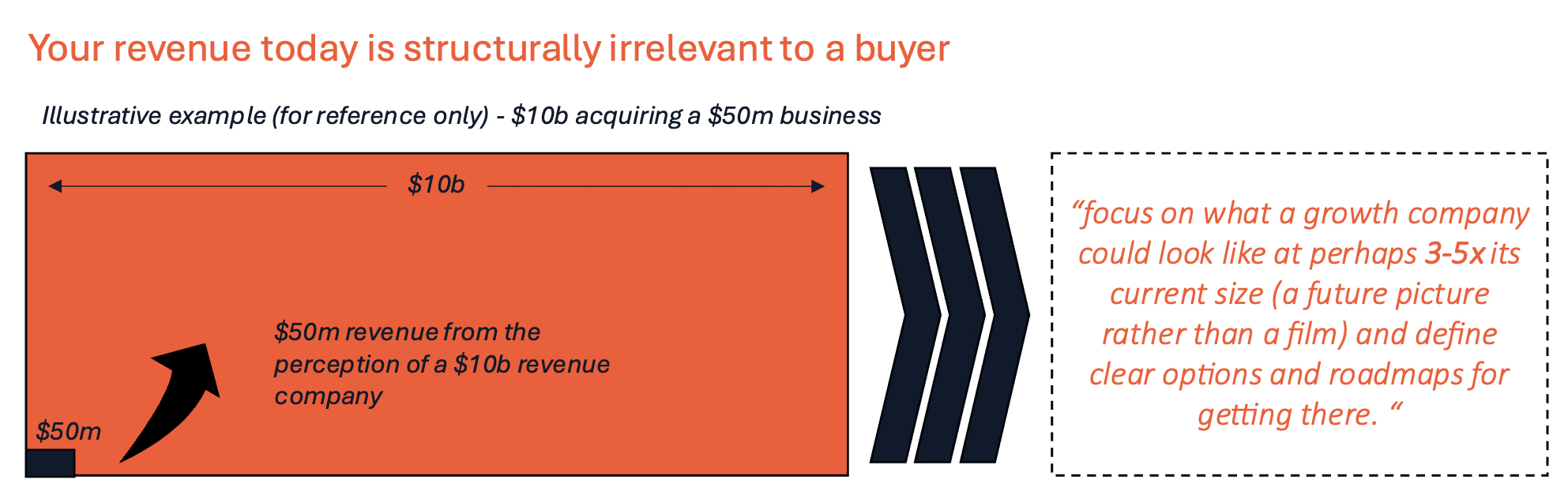

- Communicate opportunity, not (just) performance – To a $10 billion revenue buyer, any $50m revenue growth company is structurally ‘irrelevant,’ and that doesn’t change if the company grows quickly to say $75m. Large buyers are far more interested in how the acquisition can drive several hundred million in revenue and/or value post-deal, how it helps the buyer ‘fix’ a gap or problem in a business unit or enable them to compete and win large contracts or customers. No growth company can possibly know all the potential opportunities that matter to all possible buyers, but it is critical that the equity story paints a picture of how a growth company can multiply size and expand its offerings. To help expose this, we generally set aside forecasts to focus on what a growth company could look like at perhaps 3-5x its current size (a future picture rather than a film) and define clear options and roadmaps for getting there. Embedding this into an equity story already begins to reframe the discussion with buyers around future potential, not just performance.

- Expose a Company’s DNA Emphatically – Some growth companies are intensely product-focused, others are sales and marketing machines. Each will appeal to a different type of buyer. What never works is trying to be all things to all people (something many companies feel they must do to ‘ensure’ they generate interest). A compelling equity story anchors and highlights a company’s core DNA to strategic buyers who are highly attuned to this, since cultural misfit is a key reason cited when deals fail. It is critical to be clear and emphatic on which attributes truly drive a company’s success and use that to distinguish the best buyers from those merely curious. The whole process will move more efficiently, focused on counterparties who appreciate a company’s DNA.

- Use Metrics (Very) Carefully – KPIs and unit economics are VCs’ holy grails, and rightly so. But the way they are calculated inevitably involves as much ‘art’ as science. For example, how long will a current customer remain one (to calculate lifetime value)? What is included and excluded from customer acquisition cost, and over what time period is that calculated? In a SaaS business, is onboarding considered part of recurring revenue or services? The list goes on. A complicating factor is that large companies often use different metrics or calculate the same metrics differently. No growth company will ever know how every possible buyer does its calculations, but there is definitely an art in deciding which KPI’s to show and which ones to raise only later once a buyer has gained a deeper appreciation for a company’s potential. Growth companies often track far more detailed KPIs than a potential buyer (simply because they have to, given a VC or growth investor board), and over-sharing can sometimes trigger questions a buyer might otherwise not ask.

- Differentiate Clearly Vs. Competitors – We always assume any serious strategic buyer is considering as many alternatives as possible; you would if you were going to spend potentially hundreds of millions. A key element of exit prep is to thoroughly investigate key competitors and define positive differences. To be credible, this must go beyond the standard 4-square matrix where inevitably the growth company is in the top-right (best) quadrant. This level of simplicity never works for strategics who live the market daily. It is far more credible for a CEO to clearly define the 2-3 most powerful differences that make their company outstanding, and weave each into the equity story rather than only collected in a competitor slide that most audiences will discount.

- Be ‘Safe to Buy’ as well as Exciting – Many growth CEOs are allergic to the idea of being safe to buy. They spend their working lives raising excitement levels around their businesses. Yet for large buyers, safety is equally valuable, sometimes more so. How does one embed safety into an equity story? Again, there are many aspects to this but a few to think about include: if there is a full team with CEO redundancy then highlight that clearly; if a company has strong finance/legal capabilities emphasise those; if sales and contracting processes are very rigorous expose those early, etc. ‘Unexciting’ dimensions like compliance, redundancy, predictability etc. all serve to lower buyers’ perception of future risk, and lower risk always equals a higher valuation. We would argue this is even more important in the most ‘exciting’ sectors.

Communicating Positive Developments to Buyers Before a Sale Process

At its heart, Stage 1 is the ‘marketing’ phase before the ‘selling’ Stage 2. Like any successful marketing effort, this needs to anchor a few key attributes with a wide range of key buyers and repeat those until positive familiarity is achieved.

We often find a disconnect between a company’s self-perception and how the market or potential buyers view it. We also frequently encounter disconnects in a company’s own framing of its story (for example, a website might have different messaging than a research write-up or white paper, or sales teams might communicate differently than board members). Once fully aligned internally, a company’s key messages need to be broadcast to key buyers over time to increase familiarity and level-set buyers’ understanding. More broadly, we often recommend a multi-tier communications strategy along the following lines:

As companies begin intensifying their outreaches, a mutual learning and exploration process naturally starts. Buyers begin to become more aware of a target’s strategy and future potential, and a company aiming for exit begins the process of engaging potential buyers well outside an intense Stage 2 process.

A core part of our support in Stage 1 is creating those connections. This is greatly helped by the fact that the majority of corporate development (i.e. M&A) leaders are also business development (commercial partnership) leaders. Across sectors as diverse as healthcare and fintech, strategic buyers very often have the same team engage commercially and evaluate a potential deal. This sets the stage for a broader, more relaxed set of discussions where a strategic is getting to know a company both as a potential target and potential partner. Our ‘hit rate’ for curating these discussions is exceptionally high. While one reason is that our reach and network is strong, the main reason is the openness of strategics to engaging; we are generally pushing on an open door, and a well-thought-out, customised set of outreaches very often generate exceptionally high ‘hit-rates’ as a result.

In the third and final blog in our series, we will look more deeply at how to identify and curate buyer discussions, how to develop those over time to filter serious interest, and how to trigger Stage 2 through buyers who are seriously at the table.

Learn more about us.

View our transactions.