Since 2011, $60B of VC investment has gone into fin-tech globally. That’s 7,000 funding rounds, a staggering collective commitment by the venture industry to the future disruption of banking, trading and payments.

Fin-tech remains one of the most disruptive global trends, but we believe the end is near for large-scale VC investing in fin-tech. In future fin-tech will accelerate using far more strategic investment instead. VC’s should cut back their fin-tech investing significantly.

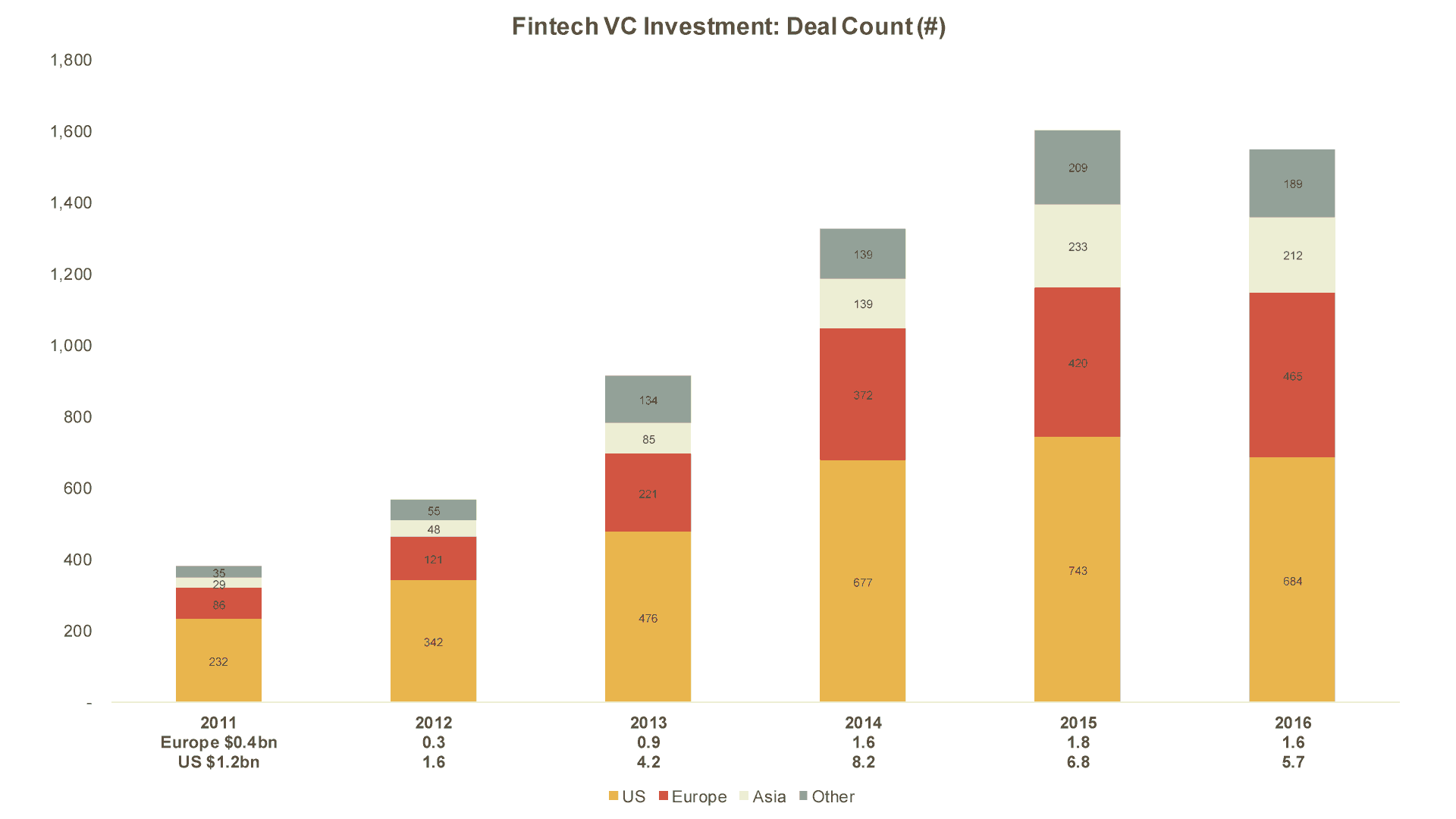

UNPRECEDENTED ACTIVITY, RECENT DIP

Of $60B of VC money, half was in the US. Europe has been only 10-20%, and Asian markets have come from nowhere to capture the rest. VC investing dipped in 2016, -15% in the US and -10% in Europe. We don’t view this as a ‘blip’ but rather evidence of a cooling off period after collective excitement in the sector drove valuations too far.

A prominent fin-tech VC said it well:

In a recent interview with Business Insider, Amy Nauiokas, the head of Anthemis Group, a New York-based venture capital firm, described the time leading up to the dip as a “period of exuberance. Big firms just sort of piled on a bunch of, let’s say, happy money,” Firms were thinking, we have money, we have capital, we have to spend it,” she said. This environment of “happy money” sent valuations for fin-techs to levels that some investors view as unreasonably high.

We don’t see the current cooling off period as just valuation driven. We believe there are long term structural trends that should bias VC’s away from fin-tech, and continue to dampen future investment activity.

WHY WILL VC INVESTMENT FIN-TECH DECLINE?

- It can take 10+ years to grow a fin-tech business that must work with incumbents, too long for many VC’s – The vast majority of fin-tech businesses must work with existing players to achieve scale. B2B businesses need to sell to large financial institutions, and even B2C businesses often must manage an eco-system involving larger incumbents. Whether in payments, clearing, or mobile banking, to achieve scale often requires convincing the largest, slowest-moving companies on earth to part with seven figures. We believe this puts back the growth curve of even the best fin-tech companies to 10+ years, well beyond most VC’s time horizon of 5-10 years. It takes a long time to train elephants.

- Customer acquisition costs (CAC) can be prohibitive – On the B2C side, there are now hundreds of fin-tech companies fighting for the same few million key customers in each geographic market; those earning over $50k, with savings, and who are open to digital financial services. The more suppliers target this group, the higher it drives up CAC for everyone. A good example: US ‘robo-advisors’ Wealthfront and Betterment are estimated to have CACs of $500-1,000, stretching their ‘customer payback’ period to 3-5 years. For many VC’s a 5-year payback period unfortunately means scaling a customer base fast means scaling it expensively, a major turnoff for investing.

- Therefore, the value of an incumbent’s customer access is incredibly high – Deutsche Bank has 30m private and corporate customers. Shell has millions of high value consumers drive into its gas stations each day. Wells Fargo does business with one in three people in the US, touching 70m people. Worldpay handles 40% of UK POS transactions. Meanwhile successful fin-tech firms mat have only 100,000 customers. With CAC’s rising rapidly, it makes sense for fin-tech firms to partner their technology with incumbents who can deliver customers for near zero marginal cost. Executing this is far from simple, but the value of customer access is rising rapidly, moving these kinds of tie ups from nice to haves towards ‘must haves’. We believe this will spur more M&A and investment interest from both incumbents and fin-tech firms.

- Broadening from single product to a digital financial services company require a lot of capital and product development risk – Nearly all ‘single product’ fin-tech companies will need to broaden into digital financial services firms. A good example is Transferwise, the $1B+ valuation FX business, that recently rolled out Borderless to hold multi-currency deposits, effectively broadening into a bank. While VC’s love to back single product fin-tech business to scale up, the magnified risks of innovating new products for new markets may make it just too risky for VC’s to follow. And the average $8m fin-tech round will have to rise to $20-30m+ to fund product broadening; not all VC’s can fund this.

- Legacy players are ‘waking up’ to the value of more rapid innovation – After years of watching, large financial incumbents are waking up to the need to partner with fin-tech firms to spur innovation. A good example of partnering benefit is in the technology development process. Incumbents have large IT teams developing software in stages, often taking months to complete. Compliance reviews only slow this further (Citigroup has 30,000 in compliance alone). By then the market has moved on, one reason so much financial IT spend is wasted.

Fin-tech firms operate a totally different ‘agile sprint’ development approach, creating products quickly, testing quickly, and refining them for release to catch market demand. Their compliance teams are a handful of people who don’t kill innovation. Buying or investing in key fin-tech firms gives incumbents a way to accelerate product development ‘outside their walls’ without having to overhaul massive internal organisations.

WHO WILL FUIND FIN-TECH DISRUPTION?

In a word, strategic investors. Its already happening.

For example, Spanish bank BBVA, perhaps Europe’s most active strategic fin-tech investor, recently increased its fin-tech fund to $250m. Ant Financial, Alibaba’s fin-tech arm, has accelerated its fin-tech activity, going after Moneygram for nearly $1B, and investing in India’s Paytm, Thailand’s Ascent Money and South Korea’s Kakao Pay. And Convoy Financial of Hong Kong led Europe’s largest fin-tech financing of last year, the €50m equity round for the UK’s Nutmeg.

In the next decade, fin-tech’s success will increasingly be funded by the most forward-thinking strategic investors, not VC’s.

Find out more about DAI Magister