A lot has been written about Uber’s latest financing round (mostly, about the reported of $50bn+ valuation), in the context of the current ‘herd’ of unicorns (apparently, 10 new horns sprouted in the last month).

Indeed, @MarkTluszcz @MangroveVC posted “Uber: $400 million in revenues in 2014, new funding round at $50 billion. Hum, let me see….insanity is the first word that comes to mind”, leading one entrepreneur to ask: “If $50bn is correct then what kind of growth rate would it need at a reasonable discount rate?”

It’s a rational question, and one us investment banker types (and growth investors too) like to answer when analysing valuations in the lack of complete data.

The short of it: you may not need to be insane, but you certainly have to believe (and the doubters would say ‘imagine’):

- First that Uber hits its 2015 target net revenue of $2bn (that’s 5x growth this year, vs. 4x growth last year, according to the WSJ) and continues to grow c. 50% CAGR for the next 3-5 years

- And second that overall tech valuations (which are at an all time high) maintain their current bouncy.

Here’s the basic methodology and assumptions:

- Let’s assume that Uber’s economics are roughly that of a SaaS company, from net revenue down. This is very much in-line with the growth equity investment approach for e-commerce and AdTech (‘these are software companies below gross profit’). We are assuming that the $400m reported is net revenue to Uber, equivalent to Gross Profit for an e-commerce company or Revenue less TAC for an AdTech company.

- Looking at the Bessemer SaaS / Cloud comps (see: LINK) we see that large, fast growth SaaS companies are trading at c. 10-15x current year revenue (e.g. LinkedIn – with a $34.2bn market cap, 36% growth – is trading at 10.7x 2015E Revenue, Workday – $18.0bn market cap, 46% growth – 14.5x and ServiceNow – $12.5bn market cap, 46% growth – 12.4x).

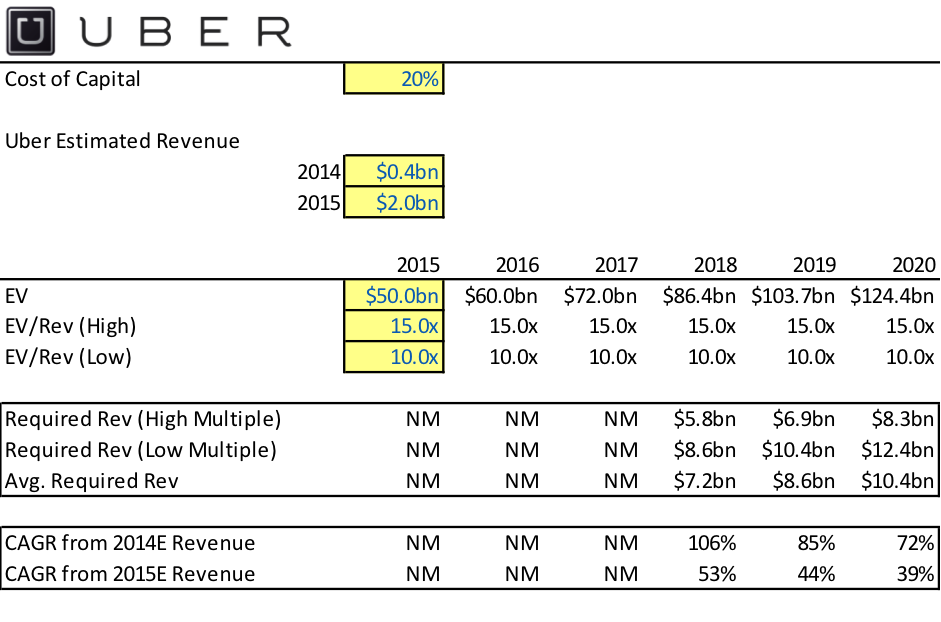

- Let’s assume a c. 20% cost of capital / target return on equity for the new investors (which we can sensitise up and down to get a feel of the range).

- One of the key assumptions (as you will see below) is the starting point for Uber’s net revenue growth, i.e. $400m in 2014 or $2bn in 2015. Now, this is certainly an area where people make take divergent views. Us investment banker types are trained to disbelieve in mythical models with accelerating growth, but then again we are talking about the uber-‘corn here.

Then the math looks something like:

(My Excel sheet is here: LINK – if you want to play around with it or run sensitivities)

So the first big bet here is, will Uber hit $2bn net revenue this year?

If it does, then it still has a lot of work to do (40-50% CAGR to justify its current valuation), but there is a rational basis for the current valuation. Let’s also bear in mind that that tech valuations are at an all-time peak, so 10-15x revenue could easily fall to 5-10x revenue in 3-5 years’ time. If valuations do fall back (which is quite likely in our view), then $50bn will look like a very expensive in-price even if Uber hits $2bn this year and then 50% CAGR for the next few years…

And if it doesn’t, well then we could hear a loud popping sound and see a few unicorns falling around us (or maybe we should say ‘the wheels falling off the Uber-bus…’).

Find out more about DAI Magister