One of the hottest areas for VC investment is AI/ML; artificial intelligence algorithms, related machine learning systems, neural networks, and back-end processing to produce insightful and self-learning applications. As nVidia’s CEO recently said:

Software may be eating the world, but AI is going to eat software

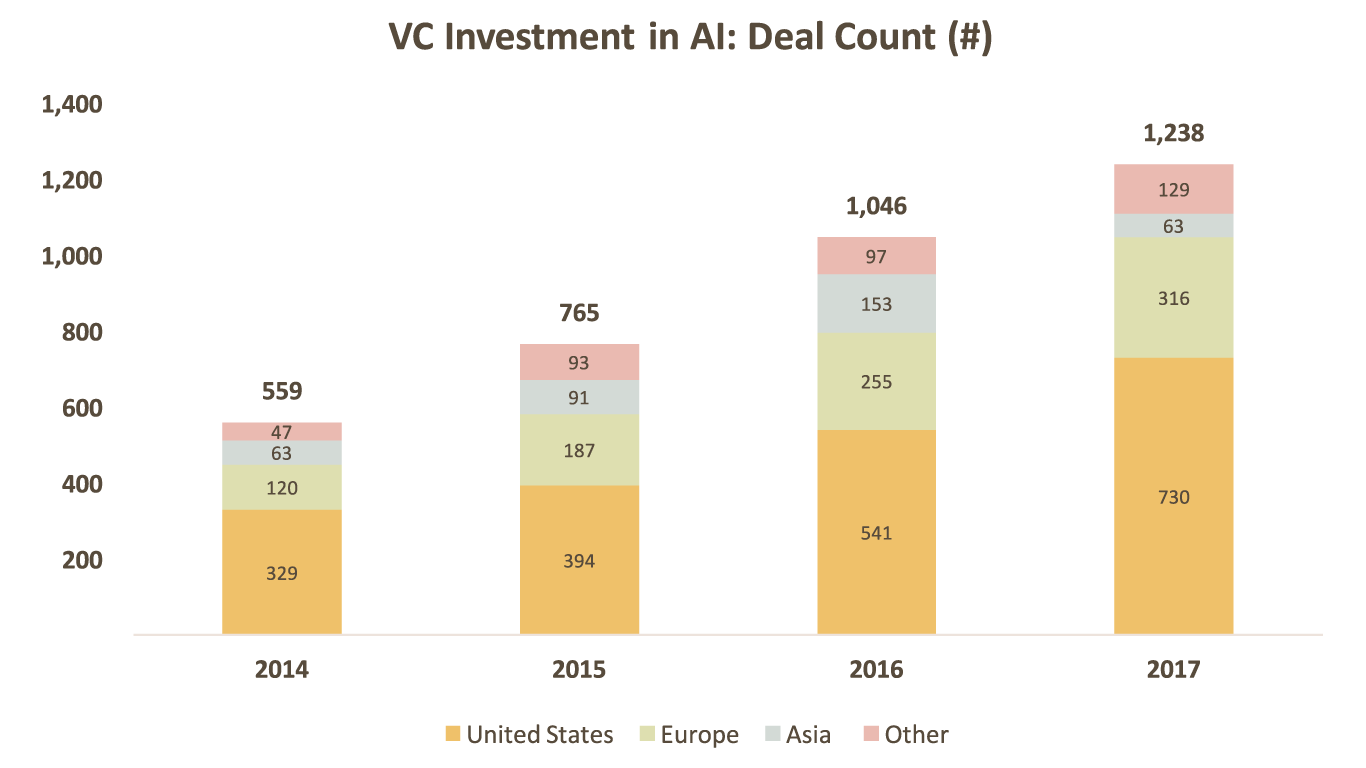

AI Investment At All Time Highs

VC investment in AI has risen from $3.2bn in 2014 to $9.5bn for the first 5 months of 2017 annualised, with the number of funding rounds nearly doubling since 2015, to over 1,200 on an annualised basis so far this year. No wonder Frost & Sullivan calls AI the hottest investment trend of 2017:

- Source: Pitchbook

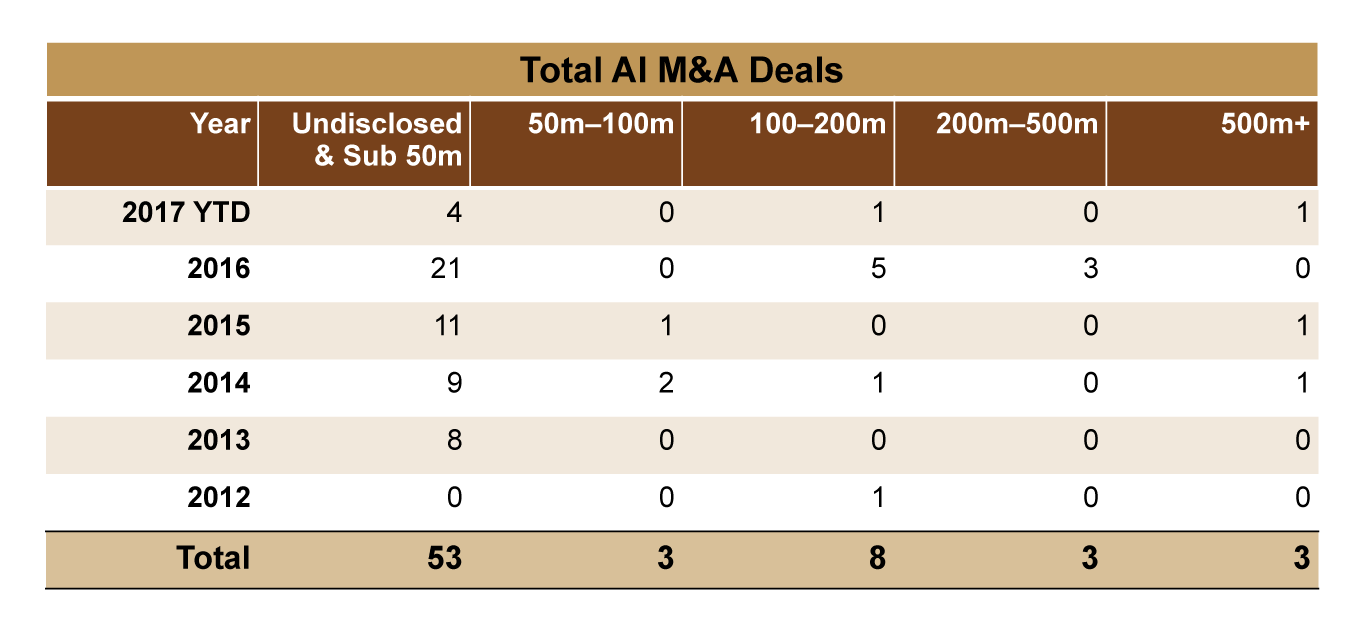

But AI M&A Is “Small-Deal M&A”

Investors piling into a space are aiming for multiple exits worth $ hundreds of millions. However, the pattern of AI exits is the opposite. Most successfully-exited AI companies sell for sub- $50m, after raising only a small amount of money. This works well for founders and small angel backers, but not for VC’s who want to invest more in companies exiting for well over $100m.

Of 70 AI M&A deals since 2012, 75% sold below $50m. These deals are often ‘acqui-hires’, companies acquired for talent not business performance. The number of $200m+ deals barely registers.

- Source: Pitchbook

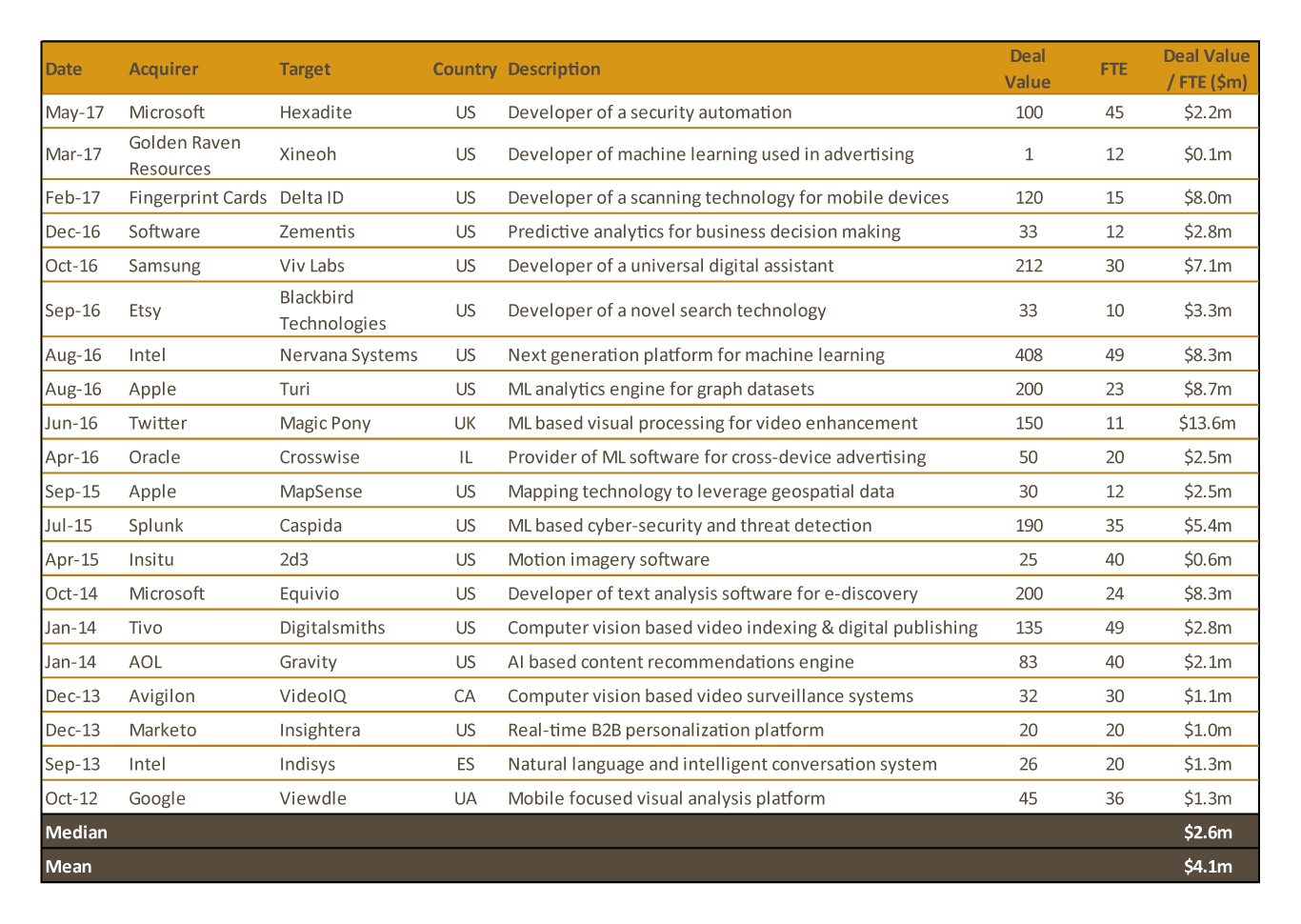

Build A 10-20 Person AI Company, Sell For $25-50M

The typical journey works like this: a small team comes together around 1-2 individuals, they forge real advances on key use cases (voice recognition, visual/video tracking, fraud detection, retail consumer behaviour etc.), sign a handful of prominent customers, raise less than $10m (often sub $5m), then attract the attention of a major buyer looking to solve that problem set. As a result, AI companies often get valued as an amount paid per engineer rather than on performance (revenue, growth, profits); the average price/employee is around $2.5M:

- Source: Pitchbook

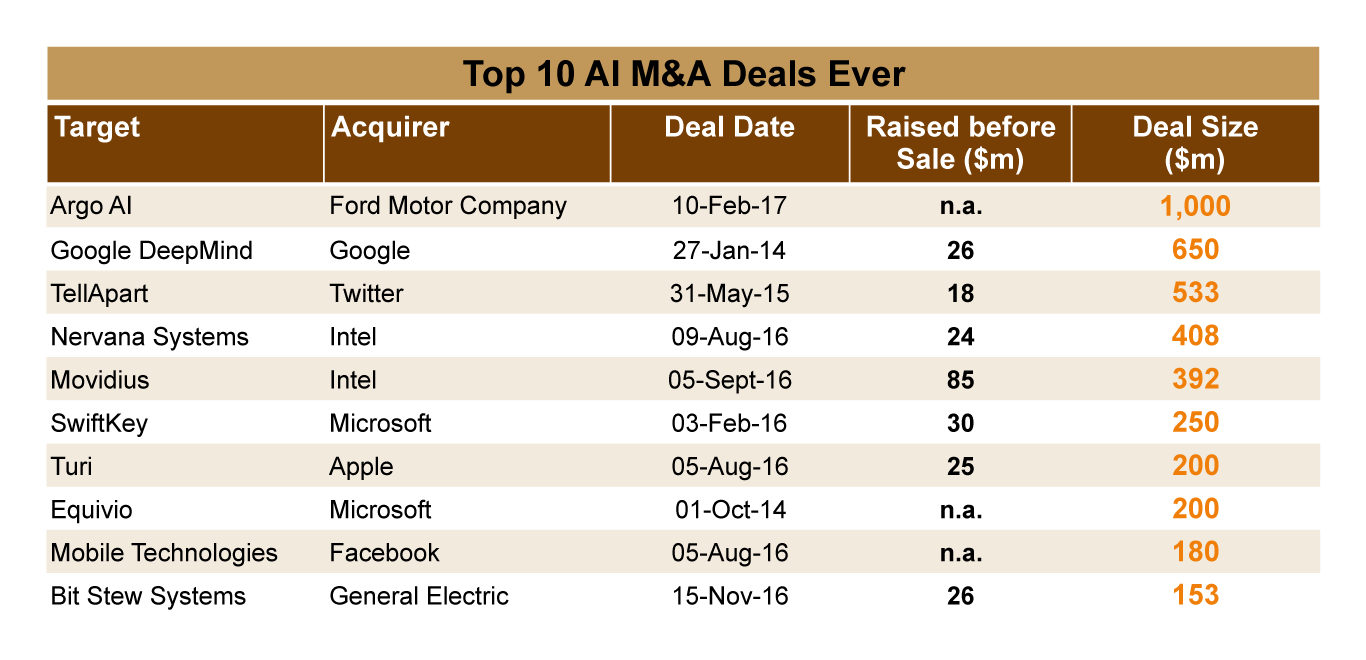

Even High Value AI M&A Targets Don’t Raise Much

The other issue for VC’s is that AI companies don’t generally need to raise much money, even if they are valued at far above $100m. Argo, valued at $1B for a majority stake by Ford, was 20 people when bought. Our research from PitchBook shows the 10 most valuable AI M&A targets raised on average only $15-25m; there was only room for 1-2 VC investors in each deal:

Sure there are larger AI companies still growing, such as Palantir, valued at $10B having raised over $500m. But a few isolated cases of $1B+ ‘unicorns’ created using significant VC money is hardly fertile ground for 1,200 VC investment rounds. The reality is AI just isn’t as rich a segment for VC’s as investment activity suggests.

In Fact, VC Investment Can Be Counter-productive

Once several VC’s invest, an AI company can no longer entertain a $50-100m M&A offer, and must scale its team and product suite to ramp to a much higher valuation years further out; otherwise VC’s cannot get the return they require. Here’s why we think this is counterproductive:

- Many AI companies’ value centres around 3 or less key technical leaders, who may not thrive in a scaling business. Often these are ex professors or deeply technical experts who can start to lose interest in a burgeoning and inevitably more bureaucratic company as it scales. The bigger an AI company gets, the greater the risk it loses the 2-3 people who underpin its value. How do large buyers cope post M&A? They’ve learned to take great care to shield these technical geniuses from internal bureaucracy, much harder when they are founders of a rapidly scaling company and are expected to have input on many key actions.

- Many buyers view the ‘scaling’ of sales, marketing and business development functions as a NEGATIVE to value. They want the technical team and the core algorithms and IP, and have more than enough commercial talent in house. They don’t want to pay extra for people they will let go.

- Raising VC money to scale an AI business forces its M&A valuation beyond a $50-$100m “tactical buy” and into a larger “strategic bet”. Buyers must think carefully about this larger bet, and this creates more risk a buyer will waver on a deal.

- For VC’s this investment profile often does not make sense. Investing in AI can mean writing a small check for a brief time to get a very good but not stellar return. VC’s want the opposite; to put more $ to work for 5+ years and get 10x their money back. It’s the difference between playing Blackjack and Go, AI M&A is often the former, VC’s always aim for the latter.

- Technical founders often don’t net any more $ after raising VC money. For example, raising $5m and selling for $50m can be far more lucrative for technical founders than raising say $25m and selling for 100m. So why should they go through the whole process? Fair question.

For many AI founders, the best approach is raising little money, demonstrating they can solve hard problems, and waiting for the M&A phone to ring.

For VC’s the best approach is often to look elsewhere.

Find out more about DAI Magister