At DAI Magister we estimate 350 European tech companies will raise €25m-250m+ funding rounds in 2021-22, a historic high for the European ecosystem that reflects a sharp rise in Series A rounds since 2017 that has continued this year even through COVID. It is a testament to the depth and resilience of Europe’s tech ecosystems that companies are still attracting record funding through this year’s increased uncertainty.

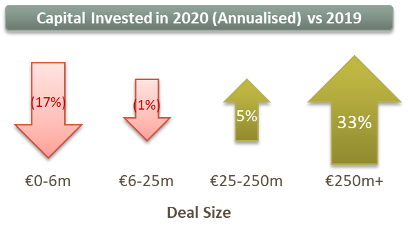

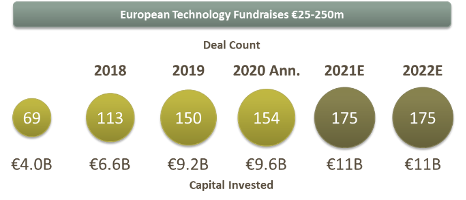

In fact, 2020 is already certain to be an unprecedented year for European tech funding, with more companies (150+) raising more money (€9.6B vs last year’s €9.2B) than ever before. For larger financings above €100m, COVID has actually had literally no effect. ‘Unicorn’ companies (valued above $1B) are poised to raise even more this year than last year’s record €5.7 billion.

Based on the record number of Series A fundraises since 2018, we estimate 175 European companies will raise €25m+ rounds in both 2021 and 2022, making both years record-setting in Europe. We also estimate 25% of these will be B2B software (both vertical and horizontal), 15-25% will be across in fin-tech (a lower proportion than previous years, reflecting caution in funding, and a shift towards less capital intensive B2B fin-tech), and the remainder broadly spread.

There are four key drivers for our forecast of record-setting fundraising in Europe:

Even though 2020 will set records, COVID has delayed a number of rounds into 2021 – 40% of European startups have reported their fundraising efforts have been delayed, and while markets remain wide open and rounds are resuming, time is required for these restarts to close. We will see the overhang effect of that during 2021, when many rounds that should have closed this year naturally spill over.

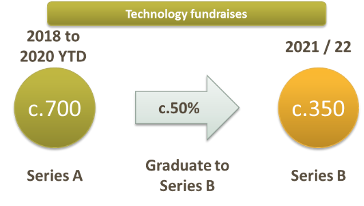

Half of 2018-20’s Series A ‘cohorts’ will raise much larger Series B and C rounds in the next two years – We have tracked c.700 companies across Europe who raised €7-25m since 2018, totaling c.€10bn and averaging €12.5m per raise. Historically c.50% of Series A companies successfully raise larger follow-on rounds, which means c.350 companies will close their next rounds in 2021-22, and some will even raise Series C money during the post-COVID window.

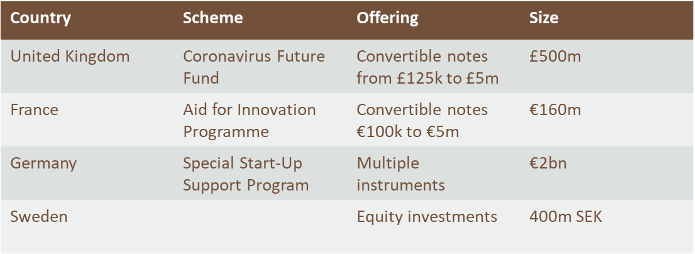

Government COVID support has funded thousands of European tech companies with convertible notes, many of which require another round in the near future – In the UK alone, aggressive government programs have supported 750 companies with ca. £1m of interim funding, and other European governments have done the same. Much of that money is in the form of ‘convertible notes’, e.g. money to support businesses through COVID that will convert into equity or be repaid when those companies raise a next round. Given the limits on public funding, we envision many of these companies will be raising money during 2021-22, as they seek to the capital to continue scaling. This is even more important for the large group of tech businesses that have benefited from COVID in one way or another. For them, major funding in the next 2 years is essential to capitalize on the market opportunity they now see.

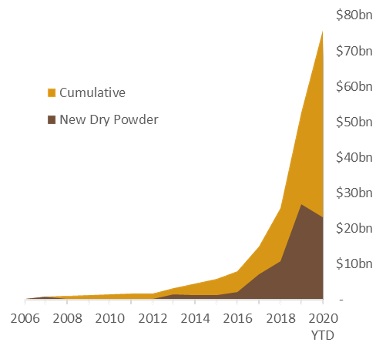

The ‘wall of money’ available from growth investors is unprecedented – DAI Magister estimate €60 bn remains as ‘dry powder’ to fund €25-100m growth equity rounds. This is an unprecedented amount of capital that is literally growing weekly. Just this month, Sequoia launched its first-ever office outside Silicon Valley in London, and Index Ventures and Summit Partners have recently raised record amounts of capital for exactly these types of rounds.

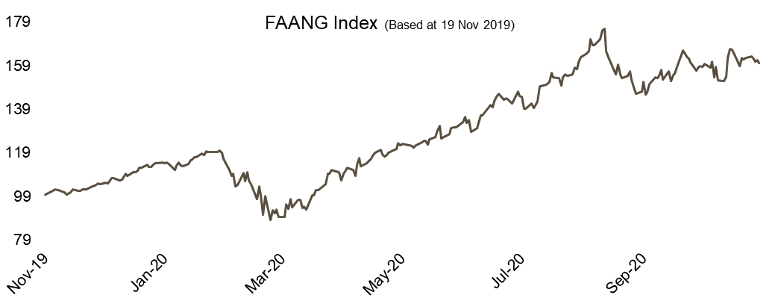

Funding activity will concentrate in sectors less-affected, or even benefitting, from COVID – Beyond the FAANG tech majors that have seen share prices soar 60% this year alone,

a large group of tech and tech-enabled businesses have benefited hugely from COVID’s disruption. From e-commerce and enabling tech to fin-tech savings and contactless mobile payment apps to logistics platforms to distance learning tools, COVID has forced nearly all EU and US consumers and enterprises to accelerate their digital shift, meaning unprecedented levels of demand for a broad group of tech growth companies. With so many European companies raising larger rounds from an unprecedent amount of available capital to back them, we expect the pace of European ‘unicorn’ creation (private companies valued at over $1b) to accelerate markedly.

In 2017, Europe recorded 22 ‘unicorns’. By 2020 that had risen to 49 pre-COVID. We expect by 2023 the figure will be over 75, reaching 100 in only 5 more years. What is already clear, even as we head into the risks of a COVID winter, is that European tech is set to accelerate dramatically for years to come.

Sources: Pitchbook, Financial Times, Many UK start-ups have less than a year’s cash left, April 2020, British Business Bank, Future Fund publishes diversity data of companies receiving convertible loan agreements, October 2020, Baker McKenzie, Covid-19 Government Intervention Schemes, CapitalIQ, Pitchbook Research, Q1 2020 European VC Valuations Report.

Find out more about us.