Software’s transition to SaaS has ramped M&A valuations of fast-growing SaaS businesses for some years now. By now, ordinarily prices would gradually drift down as ‘new’ becomes ‘normal,’ as we’ve seen recently in analytics, AI, and areas of fintech.

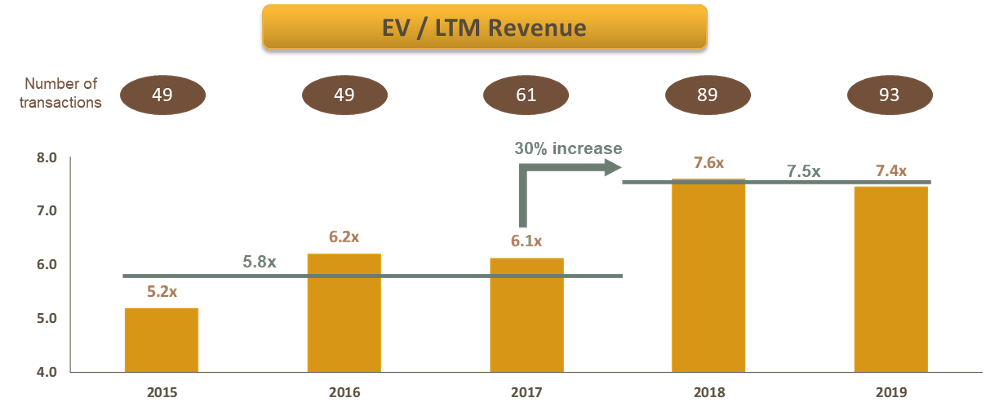

But surprisingly the opposite is true. M&A values (as a multiple of latest 12 months revenues) have jumped 30% since 2017, from 6x revenue to close to 8x revenue for deals across the US and Europe. Meanwhile annual SaaS deal count has nearly doubled to 90 deals closed a year.

We reckon there are a few key reasons for this:

Cloud has gone mainstream – five years ago people were debating how fast large companies would move to the cloud. Today, no one is. Even in key areas like financial services, companies are moving fast to shift their IT infrastructure away from on-premise. It’s a main driver for Microsoft’s huge jump in valuation, and a key reason Amazon AWS is growing 35%. The (fast) rising tide is lifting all boats.

Large software companies are buying to accelerate their own shift – It’s nearly impossible to be a software company these days without a major SaaS offering. As large software companies accelerate their move, acquisitions have risen in value as a way to fast-forward that shift.

SaaS companies have sustained rapid growth over years – Its ‘easy’ to grow 50% at $5m in revenue, but SaaS companies have demonstrated they can grow 50%+ at $25-50m or more of revenue. That gives buyers confidence they are acquiring businesses that will be able to reach $100-200m revenue quickly, which is really what software buyers are looking for.

SaaS requires more capital to scale, making M&A an attractive option for sellers – Unlike traditional software, SaaS models nearly always require more upfront investment to reap the multi-year benefits of recurring revenue. Greater capital means CEO’s and investors in SaaS businesses are always thinking about selling before a next large round, which fuels deals.

Financial buyers now ‘get’ SaaS – PE firms are the single biggest buyer category for software, typically buying more than half of all companies. Five years ago, only more specialist tech PE firms ‘got’ SaaS. Today they all do. This means that generalist funds with a focus on, say, FMCG are much more comfortable buying a SaaS business operating in that sector. It’s no longer ‘exotic,’ and that fuels broad-based buyer interest.

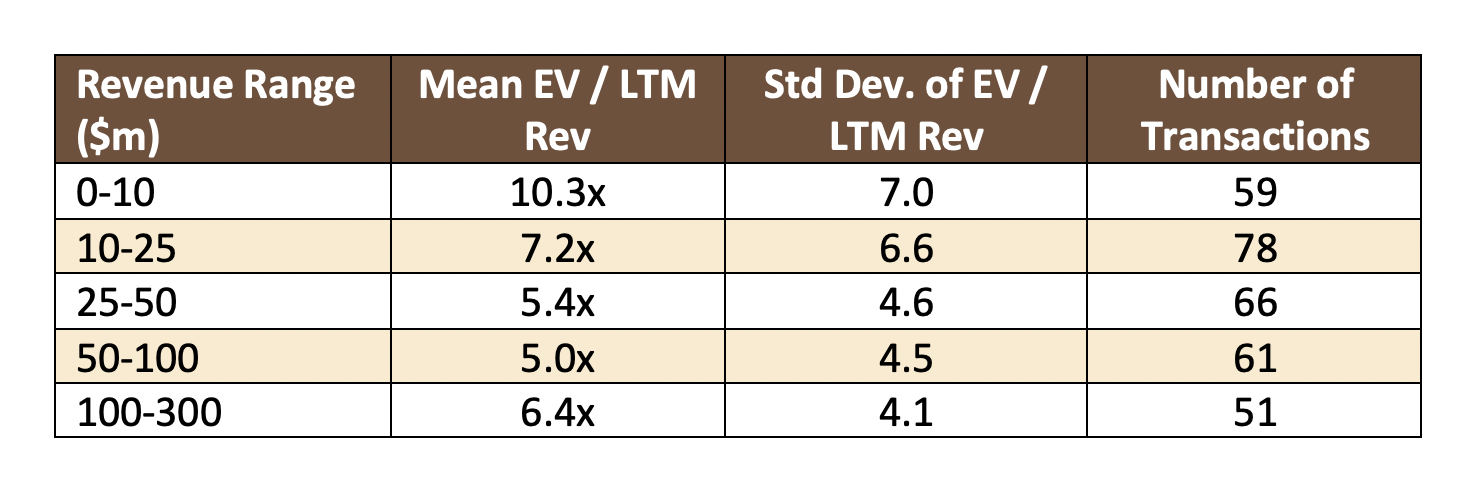

But median values never tell the whole story. We also looked at the multiples paid at different revenue levels and the standard deviations of prices paid, expressed as Enterprise Value (EV) divided by last 12 months sales (LTM Rev). Here’s what we found:

- Small SaaS companies often get 10x revenue, but there is a huge variance in valuations, as you would expect

- Those multiples drop to more like 5x during most companies’ ‘build phase (between $25 and $100m revenue)

- They then rise again to over 6x when SaaS companies grow past $100m

- Standard deviations, not surprisingly, tighten as target revenue levels rise

A main reason for the jump in valuation above $100m is the shift towards sustained high margins once SaaS companies cross into profitability. The beauty of the SaaS model is that companies can quickly shift from break-even at say $50m, to strong profitability at $100m+, often needing only 2-3 years to get there. Since even larger SaaS businesses can consistently generate 30%+ EBITDA margins, this trickles down to higher prices for those who are on the road there.

A final point is that at $100m+ revenue, many businesses have already become leaders in their niche. Most compete in specialist areas, e.g. storage, real estate, health care etc., and within their area $100m revenue is already significant. That means they are already getting the benefits of scale at that size.

SaaS companies are more valuable now than they have ever been. More are being acquired now than ever before. And the roadmap to building a high-value, acquirable SaaS business in the US and Europe has never been clearer. One would argue that far from being ‘played out,’ SaaS is only just getting started in terms of value to be created, for managers and investors alike.

As always if you liked this article, please do ‘like’ and ‘share’ it! Thank you.

Find out more about DAI Magister