While the next-gen hydrogen (H2) economy is still in its infancy, it is attracting abundant interest from strategic and financial investors alike. The current H2 investment pipeline exceeds $240bn through 2030, an investment increase of 50% since November 2021(1).

Depending on who is asked (and where they sit in the value chain), different stakeholders naturally highlight “their” technology (e.g. PEM electrolysis) as the obvious winner in an already decided race towards the hydrogen economy, citing relevant technical or commercial metrics which make their approach appear favourable.

However, as this article will highlight, technology winners are yet to emerge and various end-market applications necessitate a diversity of options, in order to encourage and then facilitate the transition.

Today, (grey) hydrogen is a captive industrial product with a still significant carbon footprint. The high costs of producing clean hydrogen have deferred broad-based commercial interest, even if the price of green hydrogen (e.g. using PEM electrolysis) is expected to fall to $2 per kg by 2030(2), driven by scale and improved technology.

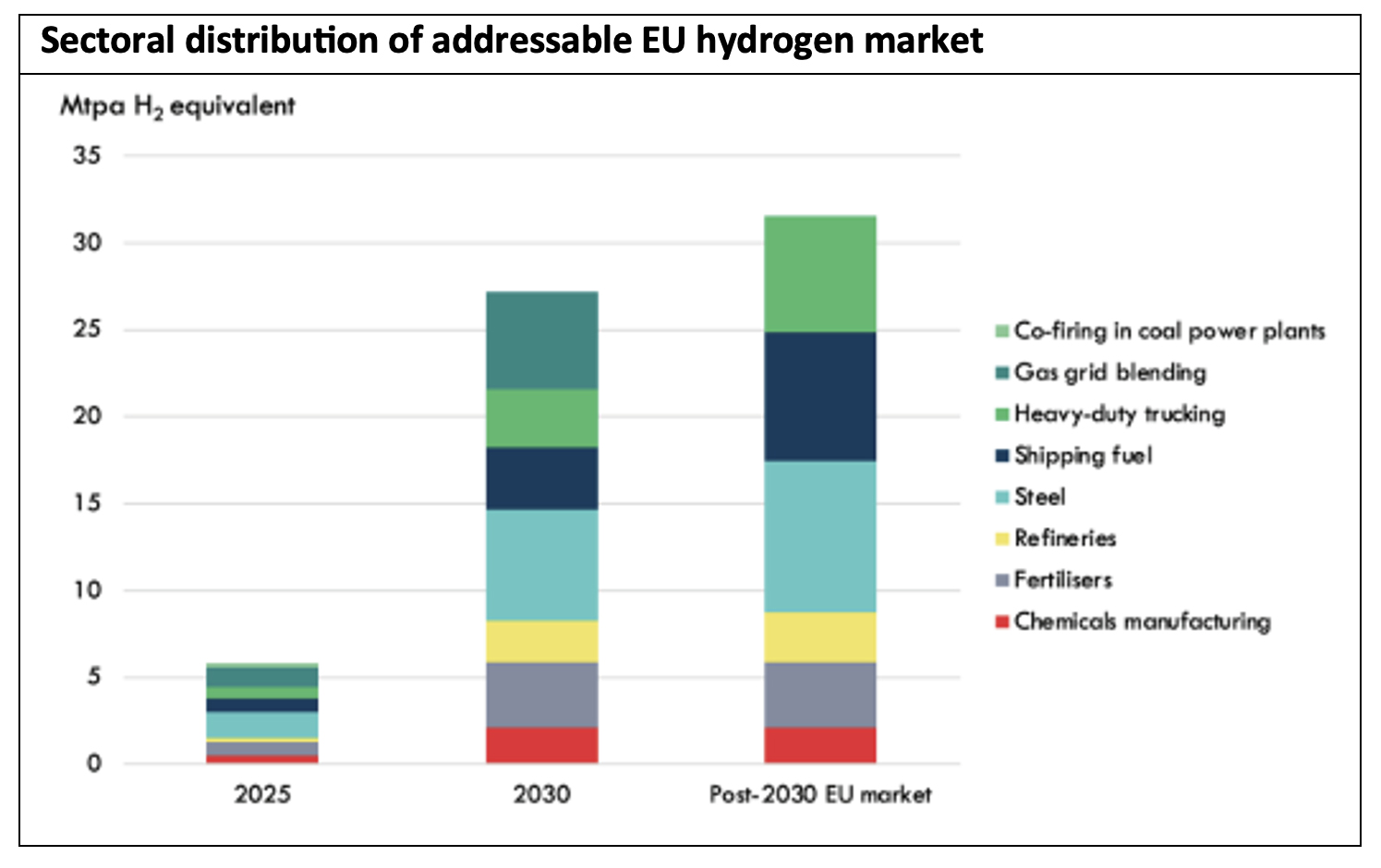

But, even if its use is limited to industrial sectors and heavy-duty/long-distance transport rather than consumer mobility, its market potential is enormous, with H2 following in the footsteps of adoption trends into wind and solar energy in previous decades. For example, a single steel plant using hydrogen instead of fossil fuels to produce iron could utilize c.300,000 tons of hydrogen p.a. ($600m @ $2 per kg), absorbing the output of 5 GW of electrolysers(3).

Keep reading and see why the growing global hydrogen economy will benefit from the advancement of a diverse range of technologies and H2 derivatives, and why hydrogen stakeholders along the value chain should be encouraged to pursue multiple avenues, in order to advance the adoption of hydrogen across end-markets.

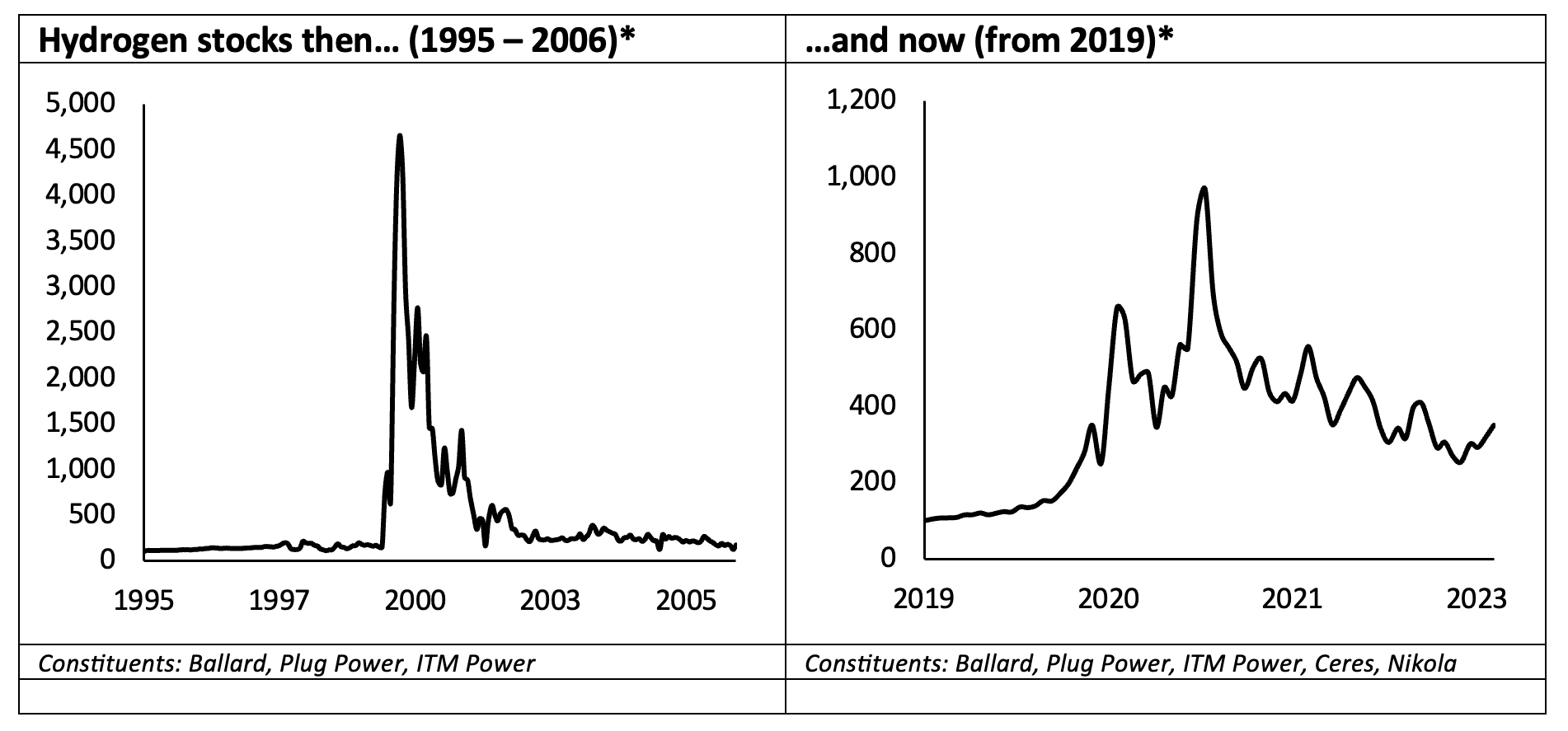

Does history repeat itself?

In the early 2000s, hydrogen stocks peaked following hype around the sector, and the same has been observed since the start of 2021; however, political motivations and the readiness of the sector are very different this time around.

Hydrogen stocks have now become an established investment class, reflected by blue-chip equity funds and long-term asset managers within their shareholder registers.

In late 2019 share prices jumped similarly to the hype in the early 2000s, but market conditions are much better this time, specifically around H2 deployment. Normalizing price levels are significantly above the post-2000-peak-period, as more established H2-players are finding solid valuation support levels, underpinned by the reality of imminent deployment at scale. As long as investors believe in a pathway towards profitability at scale, share prices should continue to find sustainable tailwinds as well.

As the main driver of hydrogen cost reduction, the feasibility and adoption of green hydrogen necessitates lower prices for renewable energy such as wind, solar. Since 2010, the cost of solar power declined by a factor of 5x, allowing technological efficiency gains e.g. in electrolysis, to drive the cost of green hydrogen closer towards cost parity vs carbon-based energy sources. Greater availability of cheaper renewable power hence differentiates the new hydrogen era from its earlier development phase in the early 2000s.

In the medium term, the case for hydrogen is expected to become viable beyond primary applications in agriculture, refining and chemical industries, and also find adoption in steel, (heavy duty) transportation, marine and energy storage applications.

Scale has been another major driver for growth, as the average size of electrolysers since 2015 more than doubled from c.40MW to above c.100MW(4). While scalability still requires subsidies to achieve H2-cost-competitiveness, governments around the world have embraced hydrogen, with more than 30 countries now publishing “hydrogen roadmaps” to support their net zero goals.

In Germany, hydrogen is the fifth most important element of the country’s annual stimulus package (just after investments into digitalisation, security). Similar to its push towards wind and solar energy in the 1990s, the German government has been a particularly vocal proponent of dedicated hydrogen legislation, calling for EU gas definitions gas to not include clean hydrogen, in order to regulate hydrogen separately(5) and independent from previous policies regarding natural gas(6) and to counter the Inflation Reduction Act’s regulatory incentives drawing H2 investment to the US.

German industry and policy makers, with a track record of spearheading hydrogen innovation within the EU, are expected to play a critical role in the development of a robust green hydrogen market, by sending clear demand signals for green hydrogen projects in the short term, supported by H2-friendly legislation.

Technology-agnostic innovation maximises progress

It is a prevailing misconception that different and parallel technological approaches towards the same goal(s) are inefficient, both from a capital allocation and resource perspective.

But this exactly is proving to be fundamental to hydrogens global success, as the numerous challenges are being met with diverse technological advances, not in lab experiments, but through different simultaneous market approaches, accelerating the broader adoption across end-markets.

As a reminder, the production of green hydrogen via electrolysis is possible through competing technologies, including proton exchange membrane (“PEM”) systems (ITM Power, Nel, Plug Power, Electric Hydrogen), alkaline (“ALK”) (McPhy), anion exchange membrane (“AEM”) (Enapter), membrane-free electrolysis (“MFE”) (CPH2) and solid oxide (“SOEC”) technology (Sunfire, Bloom Energy).

None of these electrolyser technologies have yet emerged as clear winner, as all offer differentiating characteristics including efficiency, replacement cycles, size and stackability, as well as and opex levels.

Recent pilot projects focused on alkaline (NEL/Nikola deal(7)) and PEM (Linde(8) and Air Liquide(9)), with PEM technology expected to become cost competitive with ALK by 2025, closing the current 25% cost gap in favour of ALK(10). ALK is expected to play a key role for larger projects, due to lower normalized opex levels, with PEM more commonly used for smaller footprints, due to its responsiveness to variable rates of renewable energy.

Critical innovation is also taking place on the electrolyzer component level, where suppliers of membrane technology (separating anode and cathode) (CMS, M-Power, Ionomr) are developing cheaper and more efficient technology to support the global roll-out of electrolyzer capacity.

No bottleneck from the metals market is currently expected, despite PEM representing a major new demand driver for the narrowly supplied metal Iridium. While platinum and iridium price volatility between January 2021 and January 2023 contributed to the inflation seen hitting catalyst-coated membranes, researchers at the Netherlands Organization for Applied Scientific Research have developed a method which will require 200 times less iridium in the production of PEM electrolyzers, while also improving efficiency(11).

So how do different production technologies and H2 derivatives address the major challenges facing the growing H2 economy?

The production of green H2 through electrolysis is still expensive (~7x the cost of fossil fuel-powered grey H2, with electricity constituting 60-75%) and offers poor conversion ratios (~1.3:1)(12). While mitigated through the falling costs of renewable energy, conversion into hydrogen derivatives (e.g. e-methanol (e.g. Carbon Recycling International), clean ammonia), as well as innovative waste-to-hydrogen technologies will improve end-market economics and encourage broader adoption and transition away from fossil fuels.

Clean ammonia will likely serve as a transition fuel. It can be burned directly in an internal combustion engine (ICE) with no carbon emission, converted to electricity directly in an alkaline fuel cell, or cracked to provide hydrogen for non-alkaline fuel cells. Market participants from global Yara Clean Ammonia to local producers who commonly co-locate with contracted offtakers, e.g. waste-to-hydrogen players such as Concord Blue and Green Hydrogen Technology are providing early access to hydrogen (derivatives) which can compete with fossil-based alternatives.

Another major concern around H2 distribution is the 1.5 – 5x higher cost to transport hydrogen vs natural gas, as hydrogen requires liquification in order to be shipped, increasing the cost of transport due to further energy losses(13). At current cost structures it is not feasible to ship H2 from cheaper production locations (e.g. Australia, Namibia) to expensive demand centres (e.g. in Japan or Northern Europe).

The low energy density of hydrogen, in both compressed gas and liquid forms, makes the distribution and storage of hydrogen a difficult (and expensive) problem for most applications. This limitation is felt strongly in the area of onboard storage, but it is also problematic in the final delivery and distribution of hydrogen. H2’s low energy density is also one of the greatest barriers to the implementation of hydrogen-fuelled fuel cell vehicles.

Retrofitting existing nat. gas pipelines would involve changing relevant regulations but is widely expected to be part of the medium-term transportation solution. Utilisation of industrial hubs, where (grey) hydrogen is already based on fossil fuels, including the repurposing of H2 infrastructure, offers some support and there are exciting advancements in H2 storage technologies to facilitate broader end-market adoption.

H2 conversion into derivatives (e.g. ammonia, e-methanol), or more novel technologies such as powder carriers (e.g. KBH4) or Liquid Organic Hydrogen Carrier (LOHC) forms will serve as facilitators to solve the global distribution challenge. LOHC technology, as pioneered by market leaders like Hydrogenious, allow for organic compounds to transport (absorb & release) hydrogen at ambient conditions and in liquid form. H2 transportation in powder form through a store & release agent, as developed by Israel-based Electriq, allows for higher utilization and is compatible with a range of fuel cell technologies, to turn the hydrogen back into electricity.

The debate around H2 applications has also fuelled safety concerns regarding hydrogen as a flammable gas, or its toxicity risk for ammonia derivatives. While hydrogen has been successfully and safely used in vast quantities and for decades, new end-markets which are adopting H2 as feedstock or fuel source, storage and transportation protocols will require operational adaptions to ensure safe handling throughout the supply chain.

Bright hope for tomorrow

As highlighted again and again, hydrogen properties in various forms offer immense potential to enable energy transition, and there are viable technological solutions addressing its current and future challenges. While still expensive and inefficient compared to direct electrification, it is desperately needed, particularly in sectors which are difficult (or impossible) to electrify, e.g. commercial aviation, shipping, and high-heat industrial processes.

The task to develop the optimal technology solutions and most supportive policies which kick-start and scale the H2 economy carries on, and there will be many different hydrogen value chains, competing not just on cost, but on efficiency, risk acceptance and adaptability to end-use.

But it should be clear that only the continuous innovation in diverse hydrogen technologies will create a virtuous cycle which maximizes the full range of hydrogen applications available in the future.

The $240 billion H2 investment pipeline will only be the beginning.

Learn more about us.

(2)BloombergNEF

(4)Reed Smith Hydrogen Regulation

(6)International Energy Agency

*Rebased to 100