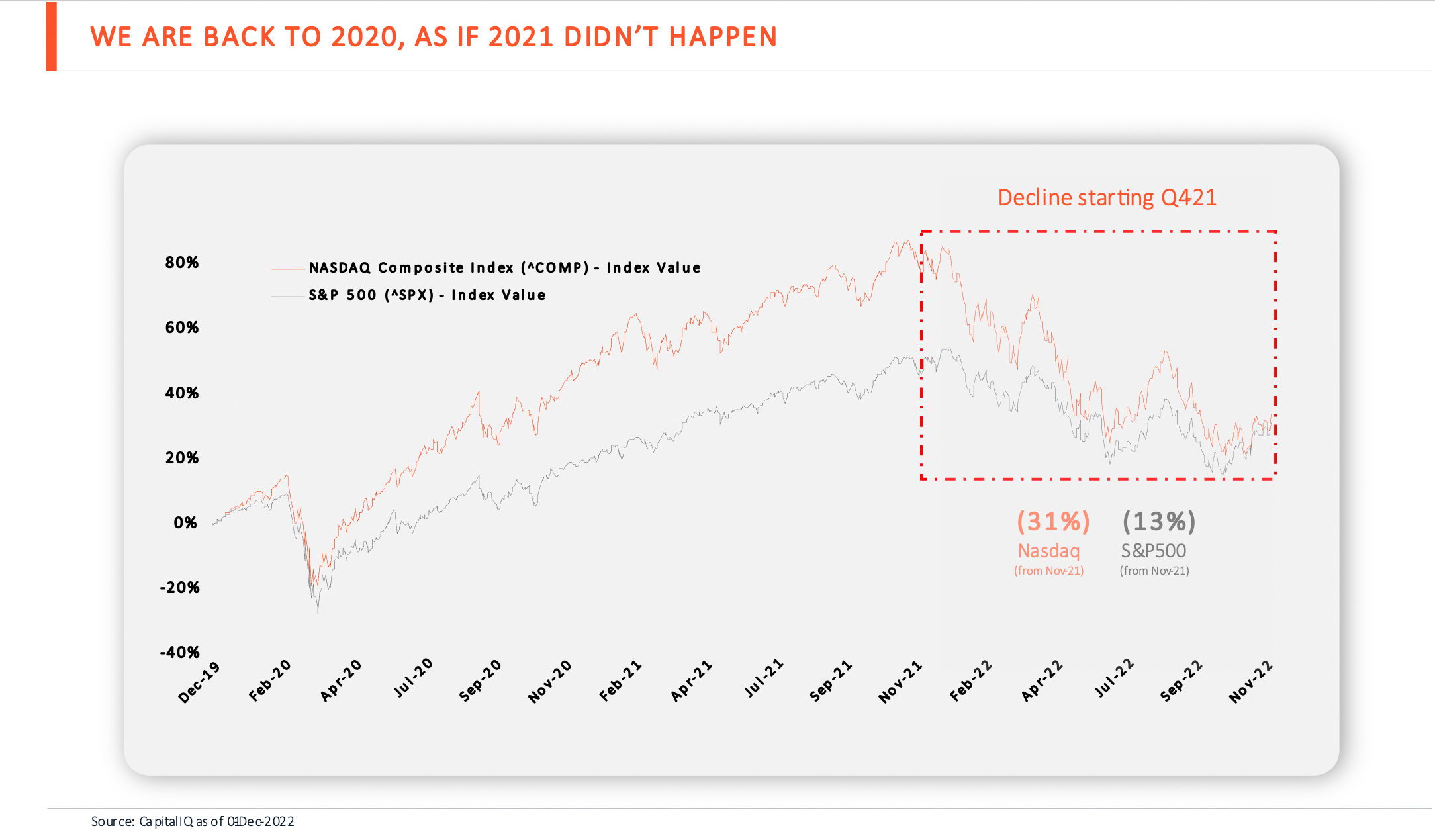

The deep freeze in tech is upon us with the markets seeing significant decline since November 2021 (see Figure 1). We are at a level last seen in 2020, as if 2021 never happened. Before the downturn, the strongest growth companies faced unprecedented choice in the types of investors they could attract due to a growth in the size of private capital amongst different investor types, looking for growth deals.

Figure 1:

The phenomena was driven by low interest rates and high valuation of tech companies in successive rounds and public markets. It was also accelerated by the 2020 pandemic, which made private equity and venture capital more comfortable at transacting further afield from home and accelerated the adoption of tech for a lock down world. The result for a company looking to attract growth capital was a multitude of sources:

- Early Stage (Seed to Series A) VCs (“VCs”): were banking on the increased valuation of their early-stage investments were able to raise larger funds and move up to offer growth equity capital ($35m – $75m rounds)

- Growth VC (“Growth Equity”): Whose bread-and-butter business was participating in $35mm + rounds were able to capitalize on the momentum in the markets to raise larger funds and do more growth investments

- Larger Private Equity players (and some hedge funds): were attracted by the opportunity they saw within tech and dropped down the size and maturity curve to capture the opportunity in the growth market

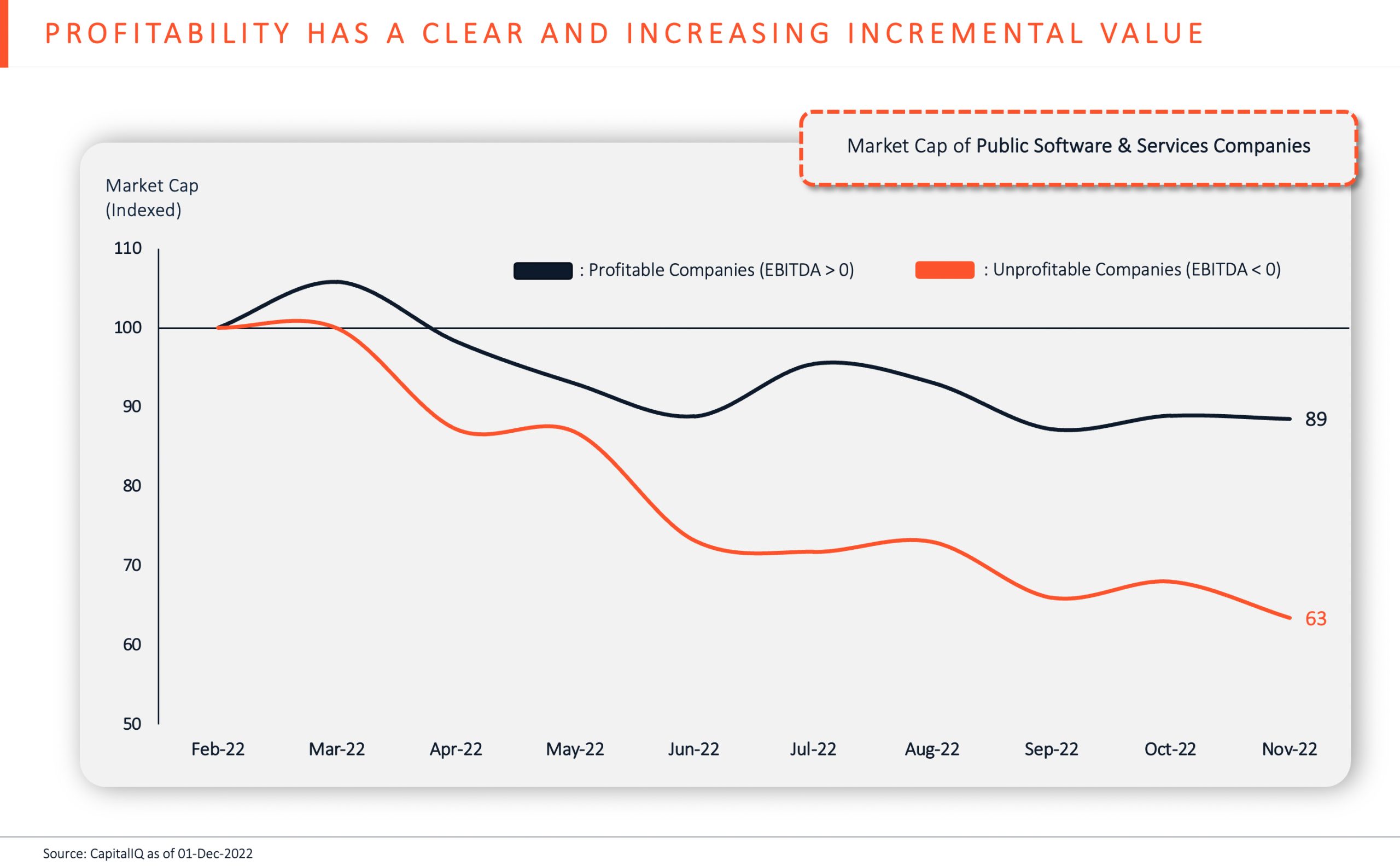

For all potential investors, profitability has a clear and increasing instrumental value. The market cap declines have been steepest for unprofitable companies through this entire downturn (See Figure 2).

Figure 2:

We expect the current environment to continue at least through next year. Recently, Sequoia’s Doug Leone observed from the stage of the Slush conference in Helsinki: “The situation today I think is more difficult and more challenging than either ’08…or 2000”. Bill Cilluffo from QED Investors commented in a recent interview that “We’re not at the bottom of activity yet. The market’s adjusted quickly, but we’re still seeing pockets that haven’t adjusted… Sometime next year is likely when we will start to see the rubber hit the road on this”. The market is today coming to terms with a new normal, which means an increase in internal bridge round, flat/down rounds and investors seeking more favorable terms (liquidation preference, redemption rights, etc.).

The current market downturn has led to a shift in the growth equity investors universe. Early VCs that moved up have now retreated to earlier stage, smaller rounds. Private Equity investors who ‘dropped down’ to chase growth and lower valuations at earlier stages no longer see growth as a substitute for cash flows. Therefore, now for growth stage rounds (Series B-C), classical growth equity is once again the investor type of choice for aspiring, established startups.

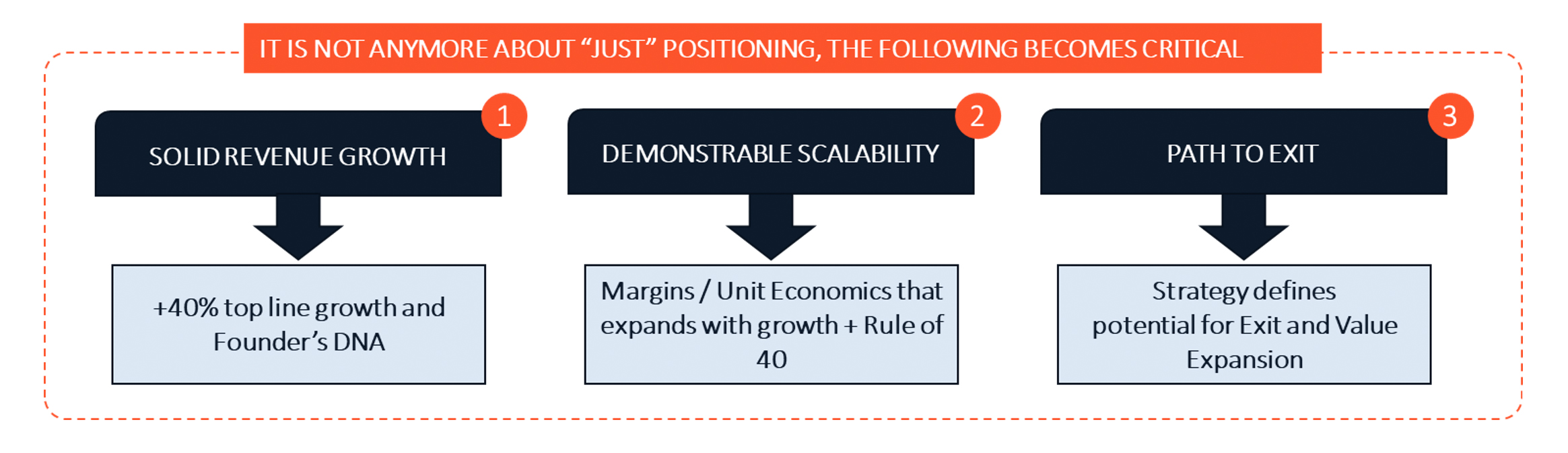

Going into 2023 and beyond, what does this mean for growth companies?

For strong growth companies, the choice has narrowed down (again) to growth funding vs PE but these two have different criteria. Very often, companies prefer growth-oriented investors for higher valuations, and the backing of ‘like-minded’ sponsors willing to support ambitious plans, whereas many PE investors remain by nature more cautious. To attract serious growth capital today, however, there are attributes companies must have:

- Revenue Growth

Investors need to see at least 50% annual top line growth for companies to qualify as growth investments. This means companies need to showcase that there is clear potential for this growth to persist in the medium term backed by a credible and executable business plan. Also, that there is a sufficient addressable market to allow for the growth and the operational or product levers the company will use to be able to achieve future growth.

- Founder DNA

Most PE investors are happy to back professional managers as the focus would be on optimizing the business operations toward an exit. For growth investors, they need to see founder DNA and ambition to solve a large problem and scale across several markets.

- Future Margins

Growth investors needs to see margins that are expanding based on revenue growth. What this translate to is a company with positive unit economics that will use the growth in its revenue base to create operating leverage on its fixed cost base. This is quite different from a business that has the potential to expand EBITDA and achieve operating leverage based on cutting costs or optimizing operations. The latter type is far more suited for private equity investors.

- Rule of 40

But growth is not sufficient. Investors want needs to see growth balanced by profitability. This usually take to form of the rule of 40 which is simply the annual growth rate of the business plus its EBITDA margin, which absolutely must exceed 40%. Investors look at the rule of 40 as a balance between the company’s growth and existing cash needs. In reality, a score of 41 is also not sufficient in today’s market; companies typically need to score 50+ with above 50% growth rates (today or visible in the near future) to convert more cautious growth investors.

- Capital Efficiency

Growth investors are focused on capital and sales efficiency once again; these metrics mattered little in the bubble of 2020-21. What sales efficiency translates into is a ratio of sales spend to incremental ARR which must be better than 1 and ideally 0.75, which means $1 invested in sales should yield at least $1 of additional ARR, ideally more. Where the ARR ‘yield’ is below 1, investors today view that company’s model as sales-inefficient, and balk at funding that (relatively unprofitable) growth.

- Valuation Expansion

Valuations rise naturally when a company can transform its positioning either through expanding its product offerings, expanding its metrics (ARPU, basket size, conversion, etc) or broadening its market (functionally or geographically). For example, a leading player within payments for the retail market in a certain country can achieve a step change in valuation if it articulates a clear plan on how it will become the leading regional payments provider across several sectors. This illustrate that the company’s total addressable market is much larger than is currently perceived and that it is capable of building a competitive advantage across multiple geographies.

- Exit Path

Today more than any time in the past 3 years, investors need to understand and see a credible exit path for their investment. Companies therefore must align the company’s strategy with the proposed exit path for the business. For companies that are considering an exit to a strategic, that means aligning KPIs with that of the potential acquirers and demonstrating how they would fit strategically with the best buyers. Companies looking to exit via IPO need to demonstrate how they will build momentum to listing, and the steps they are already taking to become a resilient public company, not just pull off an offering. It’s important to remember that growth investors can rarely exit fully at IPO, and often stay in for a long time after a listing, and their own fund returns get measured based on how well a company does months, even years, after IPO.

While the above factors can underpin a higher valuation than the previous periods, overall pressure on valuations is of course down in the current market. However, businesses need to consider that the value of each dollar raised today is significantly greater than what it was in a boom. In a tight environment, capital becomes a strategic asset that companies can use to acquire customers, talents, or competitors. In an environment where everyone is struggling to raise capital, capital is a tactical requirement, and for many companies this more than justifies raising money at pre-2020 prices.

Very often companies that do manage to raise successfully in a difficult environment are the first to be acquired for strategic prices (or exit via IPO) when the market turns back up, and this another strong rationale for raising capital today to position yourself for the upswing in the economy. Raising from growth investors willing to back a sustainable credible growth strategy puts the best growth companies on the strongest footing to accelerate their valuations, and options, coming out of the downturn.

Learn more about us.