In the past five years, there has been a sea change in the funding landscape for European tech. So much so that today many companies are opting to raise ever-larger growth rounds instead of preparing for a more “traditional” M&A exit. While this will enable a larger group of European companies to fund themselves to serious scale for the first time in history, it is already creating significant new challenges for CEO’s and fundamental issues for early backers in the sector.

Growth rounds up sharply, M&A is actually down

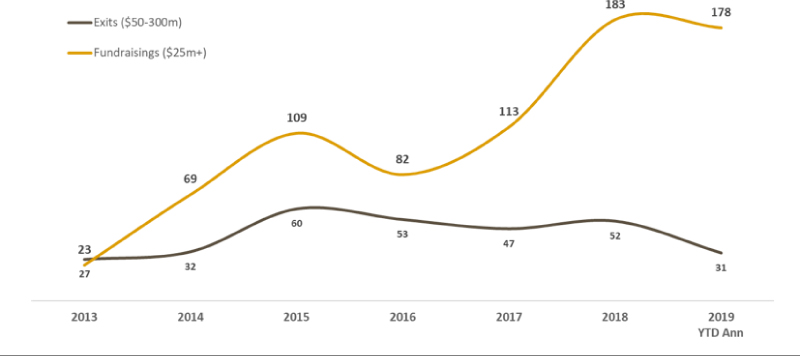

Larger funding rounds of $25m+ are up over 400% since 2013, from 40 to 180+ in 2018. This is largely driven by $25-50m rounds which have increased from 24 to over 100 in the same time period. Never before in the history of European tech has there been such a surge in available capital.

We are also seeing a simultaneous drop in European tech M&A exits for these same companies. M&A valued between $50-300m has dropped from 50+ in 2015-16 to only 50 in 2018. The two trends are clearly related. Companies are finding the capital they need to scale, or at least attempt to scale, well past a value of $300m. They are able to fund independence for far longer, aiming to achieve much higher valuations, although much later.

Key “hot sectors” driving this expansion have been fin-tech, AI and SaaS which collectively represented nearly 60% of all larger European fund raises last year, up from 25% in 2013. Fin-tech remains the driving force, but we are also seeing a sharp rise in financings for “frontier” technologies such as next generation wearables, autonomous vehicles, and more sophisticated mobile-driven gaming.

In key SaaS, fintech and AI sectors there are now emerging leaders who “happen to be based in Europe” but can effectively compete globally from a European base. The European location is incidental to their potential, and their attractiveness as a target for larger amounts of capital. With this expanded orientation, international capital has flowed into emerging European companies, and more European firms are increasing their investment sizes or raising larger growth funds alongside existing VC capital.

So, what’s the “problem”

The biggest issue is for earlier stage European VC’s who have backed companies to scale over a defined period of time (typically less than 7 years). The number of these VC exits over $50m has fallen to a point where there are sometimes only one or two in all of Europe in a six month period.

Of course, VC’s should in theory be excited by companies with greater ambition than a decade ago. And many are. But there are a growing number of earlier stage VC’s who find they have invested in companies 5-10 years on the premise of getting to an exit (90% of the time this happens via M&A), and find their investment horizons now lengthened, sometimes considerably. And given the downturn in M&A, early VC backers are finding they need to “exit” their holdings via “secondary sales”: eg selling their stakes to bigger funds as part of a large later round.

The other issue centres on founders. Many have less experience than US counterparts in scaling previous businesses, simply because the tech sector in Europe is so much younger. And if they raise a round at a valuation of say $250m, their new investors are expecting the team to scale rapidly towards a $1B value “unicorn” using the significantly greater capital base. But founders do not have anywhere near the maturity of ecosystem around them that prevails in the Bay Area, where VC is a near 50 year old business by now. And many more in Europe are first-time CEO’s because the market is at an early stage, and may not have the experience to guide companies as rapidly as large backers require.

What will be the impact?

Going forward, this “go big” mentality will inevitably result in a growing proportion of European companies aiming for, and some achieving, unicorn status on the world stage. Unicorns will come from a wide array of sectors, from FinTech to more “Frontier” technologies e.g. Wearables/Hardware, Mobile, Gaming, Autonomous Vehicles.

And while the greater flow of capital is also levelling the playing field for European competitors, rapidly closing the late stage funding “black hole” that has existed for so many years for aspiring European firms, this also means companies are raising money at a far more expensive level than before. With the far greater valuation risk today, after more than a decade of froth in both private and public markets.

Overall, we see less caution in many current funding rounds than our current point in the cycle would suggest. Companies relish raising more money, and new backers have ample funds to commit. But raising money does not mean success. And there is less prudence applied than a growing number of established European investors would like.

If you enjoyed this article please feel free to “like” and “share”! Thank you for your time.

Find out more about DAI Magister