We expect to see 8-10 notable transactions in the space and over $1.5 billion of additional investment in SSA datacentres over the next 3-5 years. African carrier neutral datacentre capacity is projected to increase 2.5x over the next 5 years, rising from 42,000 SQM to 105,000 SQM (which is worth over $900 million / year), representing perhaps the fastest growing technology sector on the continent. This is relevant for two reasons:

- There will be unprecedented investment in the coming 5 years, undertaken by a combination of international and African players. Raising capital to meet this need will create significant attention for the African data center industry, and attract a growing list of international investors to the continent

-

At DAI Magister we have identified a growing number of independent African data center companies who do not have the resources for expansion, and for whom being acquired will deliver far more value than any other route. As a result we believe M&A will accelerate in the sector from 2021

The drivers for this sharp expected increase in investment and value are already clear: There is rapid growth in the use of cloud services, which are growing at 24% CAGR ’18-’23 in Africa (faster than any other emerging region worldwide)

- Fibre infrastructure has been deployed, with a further surge in subsea fibre capacity coming through new projects underway by both existing operators, such as MainOne, and tech players Facebook and Google.

- Regulation around data sovereignty remains prominent. e.g. the Kenya Data Protection Bill 2019 requires any institution handling or processing Kenyan data to keep a copy of the data locally. This means that both enterprises and the tech giants providing the cloud solutions cannot simply rely on large scale regional datacentres alone, they have no choice but to ‘go local’ in one way shape or form throughout SSA.

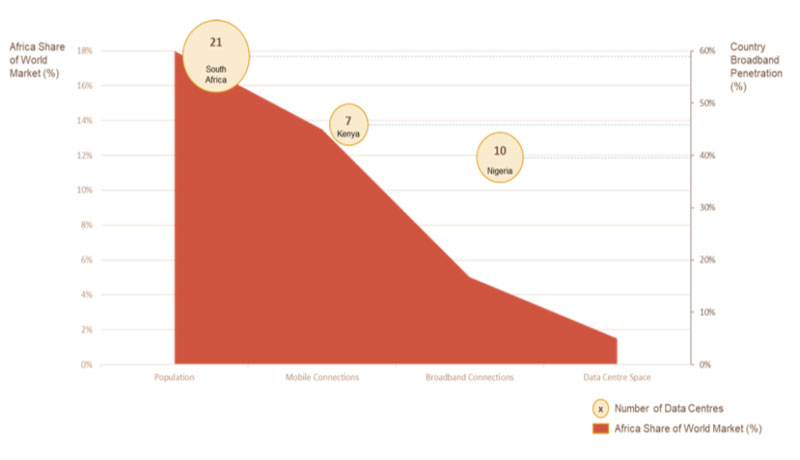

There is too little datacentre capacity to meet African demand

There is a total of 140,000 sqm of datacentre space across the entire continent, representing less than 2% of the global capacity, approximately the same as a country like Spain. Only 30% of the capacity is in multi-tenant carrier neutral facilities, and 54% of this capacity is in South Africa, followed by North Africa. SSA regional centres Kenya and Nigeria are lagging far behind with only a handful of datacentres in each. The rest of SSA will lag even further behind, as of 2019 only 13 of Africa’s top 40 broadband markets had carrier neutral datacentre.

Looking Ahead

We observe a few emerging trends:

- Shift in balance towards multi-tenant carrier neutral datacentres: If we look at the developed world, cloud services have trended towards enterprise grade carrier neutral facilities with multiple carrier connections, whilst much of the market in Africa today remains focused around Telco owned and operated datacentres. We question whether the majority of Enterprises in SSA would be willing to pay a premium for a Tier IV datacentre. The N+1 redundancy setup of Tier III is likely to meet expectations for most enterprises across SSA, with most currently used to Tier II.

- A rise in cloud services: Tech giants such as Microsoft, Amazon, Google and Facebook all require increased hosting solutions across the continent as their presence is still relatively limited today. Equally, media and content providers such as streaming services will need local caching and content delivery networks to deliver a low latency customer experience, requiring a combination of large scale datacentres and edge facilities.

- Lead times are an important factor: Datacentres have three key features; power, connectivity and security/resilience. The first two of these have long lead times, therefore capacity expansion needs to begin now despite current utilisation levels being below developed markets:

- Power capacity and provision is challenging and, depending on location, can require upgrades to central power infrastructure such as substations. Forecasts project that datacentre power consumption could outstrip overall increases in electricity generation & distribution in some countries.

- Connectivity also takes time. In markets such as London we see some datacentres directly connected to as many as 100 carriers. Whilst that degree of connectivity isn’t feasible in SSA, having multiple carriers directly link to a data centre can be a civil works challenge.

The result could be a buy and build strategy, with some companies opting to acquire, upgrade and expand existing facilities to shorten the lead time.

Conclusion

We see some clear opportunities over the next 3 years:

- Companies that can deploy with a strategic focus on creating “Data Hubs” across SSA. Locations need to intersect multiple carriers to minimise latency, increase redundancy and for close proximity to POPs and internet exchanges. Whilst the landing points for subsea cables have been determined, early movers have the opportunity to define the next wave of data hubs around which the ecosystem can grow.

- Global cloud and content providers provide strategic partnership opportunities for larger scale datacentre operators.

- Datacentre operators in SSA have to do things differently and more efficiently. Many are already starting to demonstrate an ability to be more innovative and efficient when it comes to power, using piped water, mineral baths and heat redistribution technologies in search of energy efficient cooling. This sort of efficiency will be vitally important for those looking to expand further afield given the infrastructure limitations of the continent.

Whilst there has been investment in recent years, such as investments in Teraco (Berkshire Partners) and Rack Centre (Actis) the sector remains under financed and underpenetrated, and we expect numerous transactions over the next 3-5 years.

Find out more about us