Europe has created an unprecedented number of tech companies these last ten years. Early stage money, once so hard to come by, is now 25% of US levels, an astonishing statistic given how young the European tech industry is.

Yet it is later stage money which is so crucial to creating global winners, and where so much of the real value is generated. By the time a tech companies achieves a $1B exit, late stage investors usually own most of the equity.

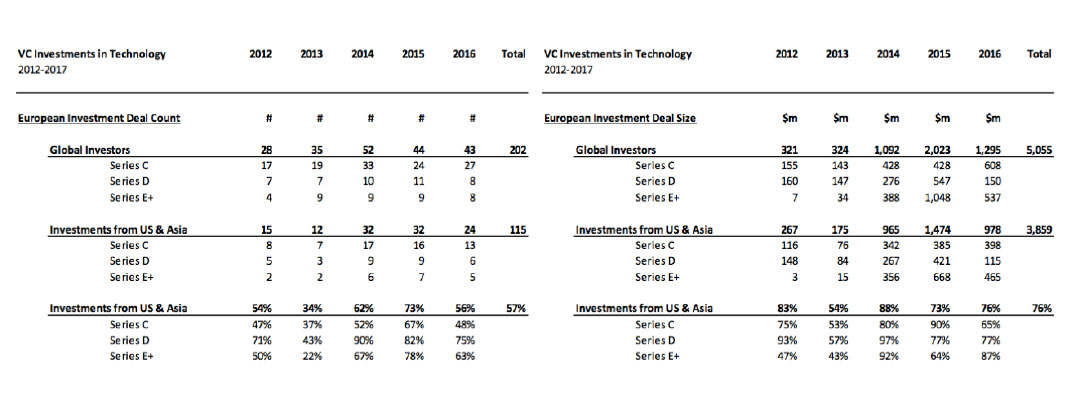

While European tech has come very far in terms of early stage money available, later stage money remains elusive for most growth companies; US tech attracts 4x the early stage money available in Europe, but 10x the late stage money.

Surprisingly, according to a recent Magister Advisors analysis, what little late stage money that is available is mainly provided by US and Asian investors. While it’s no secret international capital has been flowing to Europe in greater amounts, surprisingly over half of all late stage rounds were driven by US or Asian capital.

The impact is even greater when we look at total amount, rather than number of rounds. US and Asian investors have driven 76% of all the capital invested in European late stage tech. The largest rounds creating the biggest tech companies are driven disproportionately by international interest.

The implications are clear:

- European tech has ‘come of age’ the last five years, attracting more money from international investors overall; all signs point to this growing even more over the coming five to ten years

- Because of the lack of European late stage investors, the most promising European tech players have mainly been funded by overseas capital. While this is a huge validation of the quality and attractiveness of European tech competitors, it is also a huge indictment of the ‘local’ tech investment marketplace.

- Put simply, the quality of available ‘demand’ (companies looking for funding) far outstrips EU capital ‘supply.’. There are far too few late stage EU investment funds in Europe to fuel the next generation of winners.

- European investors have started responding. 1/3 of all $400m later stage European tech funds have been raised since the start of 2016, but the evidence shows its still far short of the available quality supply.

While the imbalance is slowing changing, we expect the number of European success stories deserving of late stage funding will double in the next years. We cannot see how the gap can be filled quickly enough by the still sub-scale European late stage sector, so unless something changes fast we expect over 80% of all capital for these companies to be driven by investors outside the EU.

Europe is now a proven laboratory for creating world-class start-ups capable of competing internationally.

However, the huge value created this seismic trend looks set to flow mainly to investors outside Europe.

Put bluntly, Europe is in the process of creating unprecedented value which the rest of the world can capitalise on.

Find out more about DAI Magister